FIIs are exiting while retail investors stay put. Will a costly market make them pay?

Aug 6, 2025 - Anurag Singh

As foreign money pulls out, domestic investors continue to pour into near-record valuations. The risk of staying invested in an expensive market is rising, what should investors do?

Indian markets are once again hovering near all-time highs — and the bullish sentiment is unmistakable. Over the past five years, the surge has been nothing short of spectacular. Nearly 18.5 crore demat accounts and over 5 crore unique mutual fund investors have joined the party — both numbers having grown fivefold since 2019. With India’s young demographics, many expect this investor base to expand further.

While the past year’s returns have been somewhat muted, most see it as a brief pause in an otherwise strong bull run. Yet, amid the euphoria, there’s one group that seems to be stepping back: foreign institutional investors (FIIs).

FIIs have pulled out a net INR3.1 lakh crore over the last 12 months (as of June 2025), even as domestic institutional investors (DIIs) pumped in INR6 lakh crore, according to media reports. FII ownership now stands at around 15% of India’s listed market cap — down sharply from the peak of nearly 23% in FY14. And this selling streak has only intensified over the past five years.

For many retail investors, this is baffling. Why would anyone exit when the music’s still playing? Isn’t this a time to make easy money?

Seasoned investors, however, are less surprised. It helps see things from the other side. If you’re heavily invested in India, this perspective is worth understanding. Enjoying the rally is one thing. But it’s equally important to grasp why the sellers are walking away. And the most obvious reason? They have options.

Nifty vs. other emerging markets returns

The biggest degree of freedom FIIs enjoy is the choice of markets. They are not tied to one market only. Examine the returns from some comparable markets for the H1 of 2025.

Nifty grew by 8%. Remember, India also levies capital gain taxes on FIIs so this number will appear lesser. Compare this to 33% index returns in Taiwan, 22% in Hong Kong, 20% in Germany, 27% from Korea and 15% from Mexico. So, it was a wise choice to move away from India and invest in other markets that were undervalued. Because expensive markets eventually moderate in returns. And foreign investors understand this better than someone who is invested in one market only.

Higher valuation of India against others emerging markets has been evident for quite some time now. Most of these markets have had a trailing P/E ratio ranging from 12 to 15 at the start of the year. Compare that to India’s persistent valuation multiple of 25 plus. It was just a matter of time that high valuations resulted in poor performance. You can’t buy expensive and get away for long unless the growth keeps up. The equation becomes unsustainable after a while. Thus, for those who keep selling a bullish narrative, just be aware that they don’t have a choice of markets. You do, at least to invest or not to.

But why have Indian valuations skyrocketed? The answer also lies in the choice. The government, like with everything else, has restricted your choice too.

Capital controls create inefficient returns

Free market leads to fair price discovery. Capital controls result in poor market dynamics and inefficient prices. Most developed markets don’t have such controls, which allow their funds to invest freely across the globe. This prevents overheating in stocks and keeps valuation fair and market driven.

Indian funds, however, are not permitted to invest in foreign markets. The one-time limit of USD8 billion was permitted but got exhausted as soon as it was created. It has not increased since. Compare this with the flows of nearly USD50 billion that Indian investors are pumping to markets every year. This capital restriction didn’t matter in the last decade as the market was sufficiently balanced on fund flows and prices. But in the past five years, it has created a bubble of sorts.

Consider this: The total equity AUM (asset under management) of mutual fund industry in 2005 was INR60,000 crore. Now we get almost INR26,000 crore every month. As per AMFI data, the AUM of the Indian mutual fund industry has grown from INR10.8 lakh crore as on March 31, 2015, to INR69.5 lakh crore as on April 30, 2025. That is a 6.5x increase in 10 years. That is a CAGR of 20%. The earnings growth doesn’t compare to this. Nifty 500 EPS grew from INR305 to INR900 between January 2015 and January 2025. This comes to a CAGR of 11.4%. So, the fund flows have grown at almost twice the rate of earnings growth. When this happens for a decade, the prices hit the ceiling because the funds are buying the same stocks at higher prices. Not because they like the stocks. But because the fund inflows force them to buy, whatever the price.

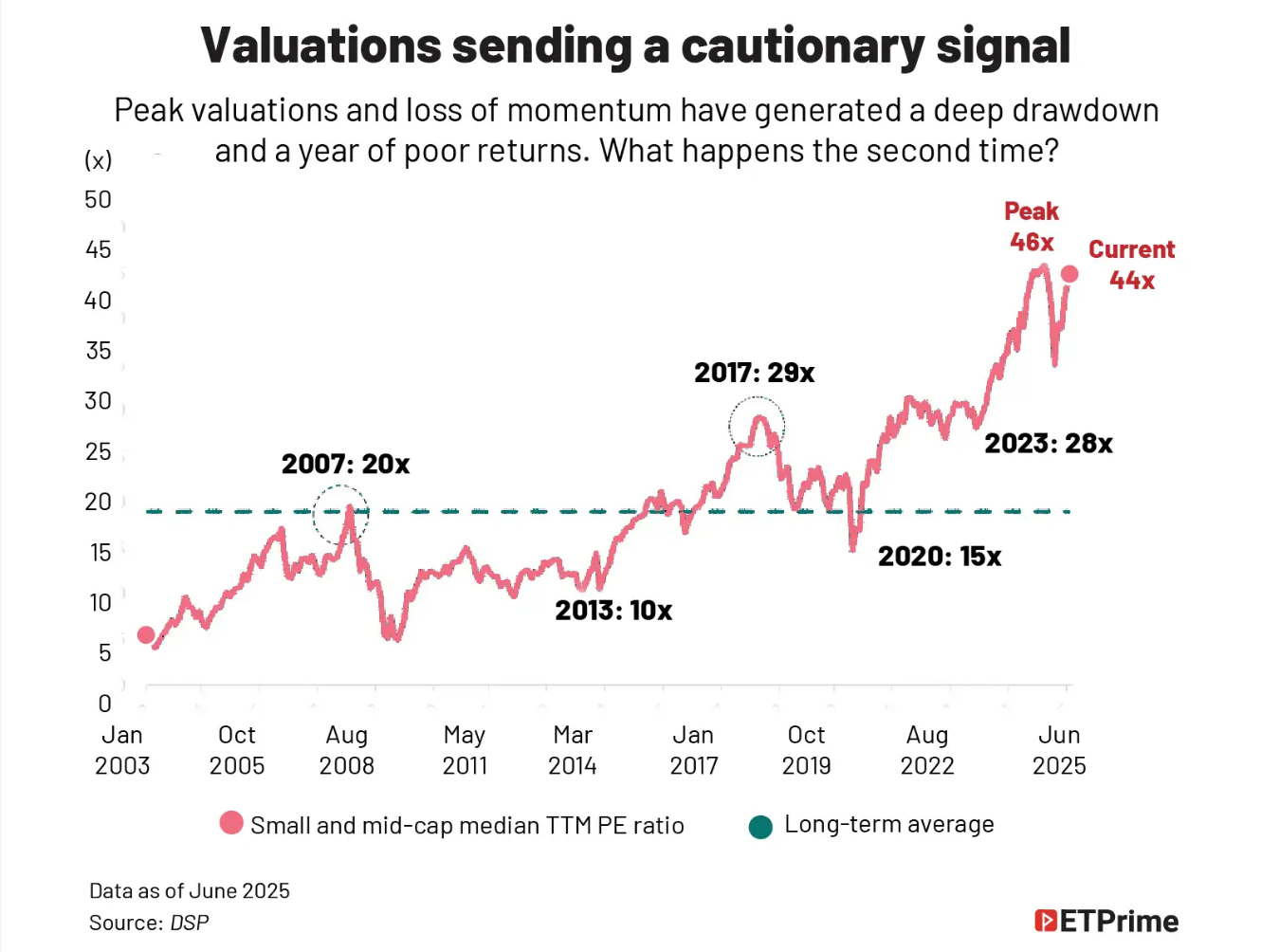

So here we are. At the peak of September 2024, 50% of NSE 500 stocks were above 50 P/E multiple. This is unheard of in any major market. The trailing 12-month P/E multiple for all mid and small caps within NSE 500 is now at a super-expensive 44x. This was mere 20x in in the last bubble of 2008.

The biggest beneficiary of this is the current stockholders. No wonder, FIIs and even promoters are constantly selling. The only buyers are the DIIs and retail investors. They are in relative returns business, not absolute returns. Funds have to outperform the index on a relative basis only. As the notable fund manager Sankaran Naren recently said — all risk lies with the investor.

This is going to have much larger ramifications for Indian markets and your SIP returns — much more than people are talking about now.

What should investors do?

Indian investors need to appreciate that crowding out doesn’t create good returns. It is far too common now to assume markets will provide superior returns. It may turn out a bit different now since the fund AUMs are growing faster than earnings. The money ideally should chase global markets to invest but this is not permitted by the Reserve bank of India. This has taken stocks to very expensive levels and may result in sub-optimal returns for investors in near future. As of now, that looks like sub-10%. For anything more, you’ll have to work harder at active investing. Mutual funds won’t be able to do that for you since their relative performance stays broadly around the index.

There may be a time in future when everyone gets scared. It is hard to imagine but those moments arrive in every market. And it would seem like markets are a sure place to lose money. That’s when you need to invest more, knowing well that you may lose money before you gain. And contrary to today’s narrative, there will be no guarantees. So, you buy when most people are bearish on stocks. That’s when real money will be made. This is not that moment. Thus, wait with caution. Don’t throw good money after bad. To get rich fast, go slow now.

The article first appeared for The Economic Times in August 2025.