SIP investing for 20 years may not multiply your wealth

Sept 12, 2024 - Anurag Singh

The second of the three part series highlights the pitfalls of passive investing style associated with systematic investment plans. It analyses whether SIPs have potential going forward.

The first of a two-part series highlights the pitfalls of passive investing style associated with systematic investment plans. It analyses whether SIPs have potential going forward.

There are few challenges though that need attention.

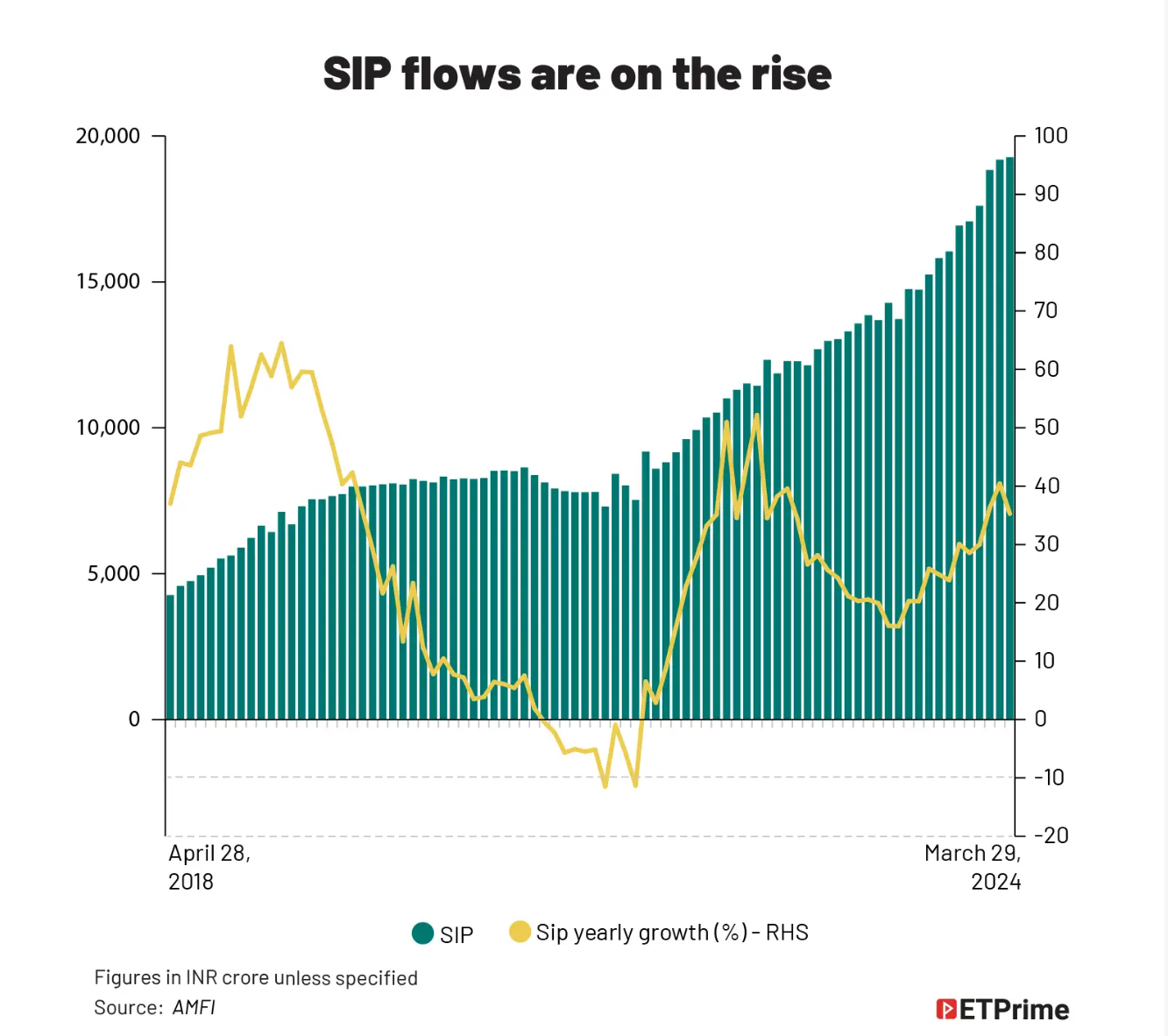

Firstly, most growth in new SIP accounts happened in 2021 when markets were at peak valuations. Flows per month peaked in October 2021 just as the markets did then. So marginal money is trying to time the market even on SIP mode.

There is another side to the SIP story that is concerning. SIPs are getting closed at rapid pace indicating lack of conviction by almost half of the customers. The FY20 had a total of 31 million SIP accounts. This increased to 63 million by FY23 and 83 million by FY24. But to get to the additional incremental 20 million SIP accounts, the industry had to open almost 43 million new accounts. So, almost 23 million accounts were closed or deactivated.

That implies that a good 25% of overall SIP accounts base were closed in last one year. Even if these folios closed and moved to another fund, the trend is defeating the purpose of SIPs.

Is the SIP story real or just another flavour of chasing returns if the going is good?

So how many unique customers have stayed since 2020? Research on that is limited. Certainly, much less advertised by fund houses that have folio-wise data. But there is a new twist that may ruin the SIP story in unexpected ways. It will also test the patience of committed SIP-pers in ways not seen before.

Chasing past returns?

New SIP accounts are closely linked on the movement of the Nifty 50 and have a very strong correlation or R square of 75%. For every 10% move in the Nifty, SIP flow will likely increase by 9.2%. But what is more interesting is that if the market goes flat or simply doesn’t move up for say more than a year, the SIP flows will begin to dip immediately. Let’s examine this a bit more.

Transport yourself to 1997 now. An investor would love to capitalise on markets. The mutual fund distributor pitches him the virtues of long-term investing and how the “India story” is shaping up. Yes, that’s true. Some of the current readers may be surprised to hear this but there was an India story even then. It has been there all the time.

You are about to sign the papers. But you ask for past returns CAGR for Nifty and the fund performance. The broker is not very keen to pull out that underwhelming chart hidden somewhere in the back of his files. You insist.

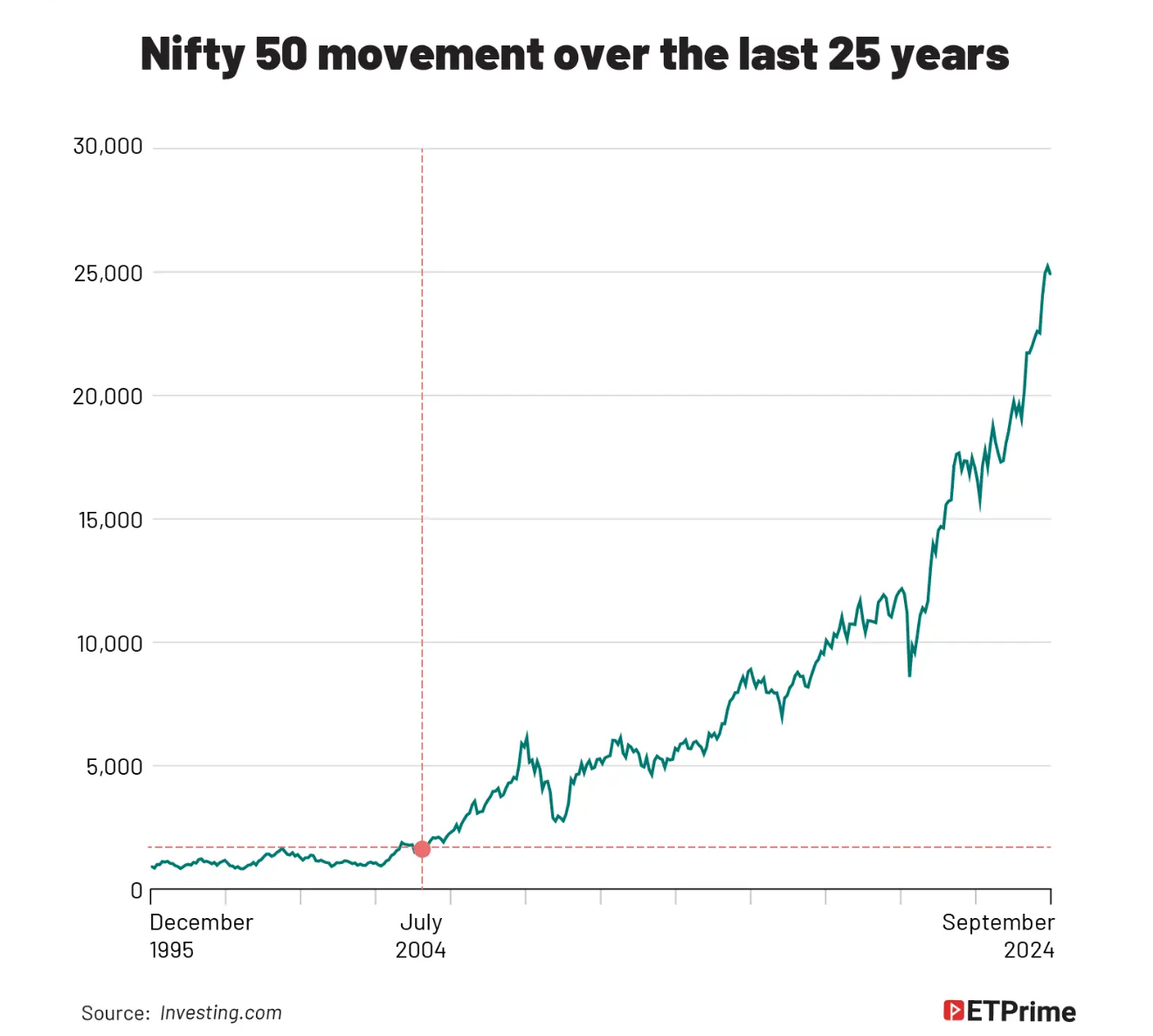

Here is how that looks like. The past three years Nifty returns (1994-97) are exactly zero. Nifty was launched in 1994 at 1000 and by 1998, it was back at 1000 after a few attempts to 1150 or so. The fund performance, even worse. Well, do you want to make that SIP now?

Remember – this is 1997. Fixed deposit rates were 12% or more depending on the bank. Who would be crazy enough to buy mutual funds! Markets are not for me, you say. Well, that explains why you don’t come across people who bought those funds in 1997 and even less who stayed. Conventional wisdom was not in favour of the markets then. Past performance didn’t support any optimism.

And that also explains why the conventional wisdom is against the FDs today and supports the markets. But have three years of negative market returns and then we can talk.

The final cut

Historical challenges seem easier if they’re viewed from today’s lens. And almost everyone from the past era appears foolish in light of what you know today. Recency bias and nominal return traps can distort your perception of future returns. Every generation has faced these issues. It is unlikely that this one does any better. In fact, all indications suggest otherwise.

Since inception, Nifty returns have been 30x in 30 years. It looks impressive. However, simply adjusting for inflation, the index would have been at 7000 on nominal basis today. So, the real returns are just 3x of the original level, a stark contrast from the nominal returns at 30x. Back of the envelope calculations show the real returns CAGR on Nifty since inception comes to 4.5%.

Believe it or not, this is very impressive. And unlikely to be repeated. I have discussed why in my first article in decadal returns in Indian markets. We’ll be very lucky if we can get even 4% real returns in the next 25 years.

Retrospective analysis can be helpful but has limitations. You can’t pick great investment ideas with retro analysis. If you do, you can’t be sure they will succeed. In most cases, they won’t. Else, investing becomes too easy like a math formulae. And everyone would be a great investor. If only.

The article first appeared for The Economic Times in Sept 2024.