SIPs of a hot market can’t save you enough for retirement

May 15, 2024 - Anurag Singh

Retail investors are chasing high markets through systematic investment plans (SIPs). However, recent data indicates that this will not end well because expensive markets always lead to lower returns.

Systematic Investment Plans (SIPs) came into existence to beat the market volatility and timing disasters. The experience, however, is that they are creating the same old issues of poor timing and crowding out based on past returns. SIPs looked like great investing tool in hindsight as there were none in the past. They may not look great in future as there are too many of them now. And the data is deteriorating fast.

My recent visit to India was an eye opener. I met many promising young men and women who are regularly saving and contributing to SIPs. They’re not rich today but are certainly hustling it out. They deserve credit for that. In fact, that is not new for any young aspirant who appreciates the merit of education, hard work, and persistence. And where there are aspirations, there are goals too.

Most financial goals are versions of this theme – I need to have INR5 crore by next 10,15 or 20 years. For others, the sum is even higher to the tune of INR10 crore or INR20 crore. SIPs are planned accordingly. Since the corpus depends on higher returns, the tendency is to drift towards mid- and small-cap funds based on historic performance.

Almost everyone I spoke to believes that markets nearly assure you 14% returns at index level. But why accept low returns when you can make more? The young ones believe it is smarter to invest most of SIPs in small-cap or sectoral funds. Plan is to make 20% CAGR or more.

This because of the common belief — this is India’s time or India has arrived, etc. There is very limited scepticism about this theme.

How much is enough to retire?

Are these return assumptions realistic? If the formulae to get rich was so simple, why is it that very few from the previous generations have corpus of INR10 crore from market investments today? Very few in our close acquaintances have made wealth that way. Were earlier generations less smart or was that not India’s decade? Isn’t that a fair question to ask?

It may be worthwhile to recall that the decade of 2000s was the best time ever for market returns as I analysed in my article about decadal returns.

Part of these ambitious goals can be explained by the age phenomenon that self corrects with time. In the USA, a study by Northwestern Mutual indicates the boomer generation that are now in 60+ group believe that USD1 million (INR8.4 crore) is enough to retire. The Millennials and Gen Z believe the number to retire comfortably is USD1.6 million plus.

One overestimates the wealth they can create when young. As they grow older, people try to bridge the gap between optimism and realism. Still, estimates in India are very ambitious. Where does that come from?

SIPs: The new panacea for retail investors

The mutual fund industry has forever struggled with erratic flows. Global experience is that most retail money gets raised when recent returns look great, but markets are near the peaks. This results in further inflation of valuations until the system breaks down to get a reality check. The next few years are painfully slow and most money pulls out at losses. Some of these investors probably never return to markets. It becomes a huge marketing challenge to solve for the problem for bulk fund flows at the wrong times.

Mutual funds found a solution to this in SIP, inspired by the 401K plans revolution in USA. Contribute every month to the future funds that are mapped to passive index funds. Research was produced that inspired confidence on cost averaging when buying in small bites every month. The pitch from brokers starts like this – had you invested in such and such funds via SIP route since 2002 (you can’t go wrong starting from there), your funds would have amounted to XYZ value. This number is always tempting, no matter who you are.

If this is the performance in last 15 years, why can’t the same repeat in the next 15? SIPs started selling like hot cakes. What’s better, the fund managers were able to rebut the long-standing challenge with equity investors — the one of short-term volatility and losses. Now if the market corrects, you justify the SIP cost averaging even more. What could go wrong?

Where is the SIP discipline?

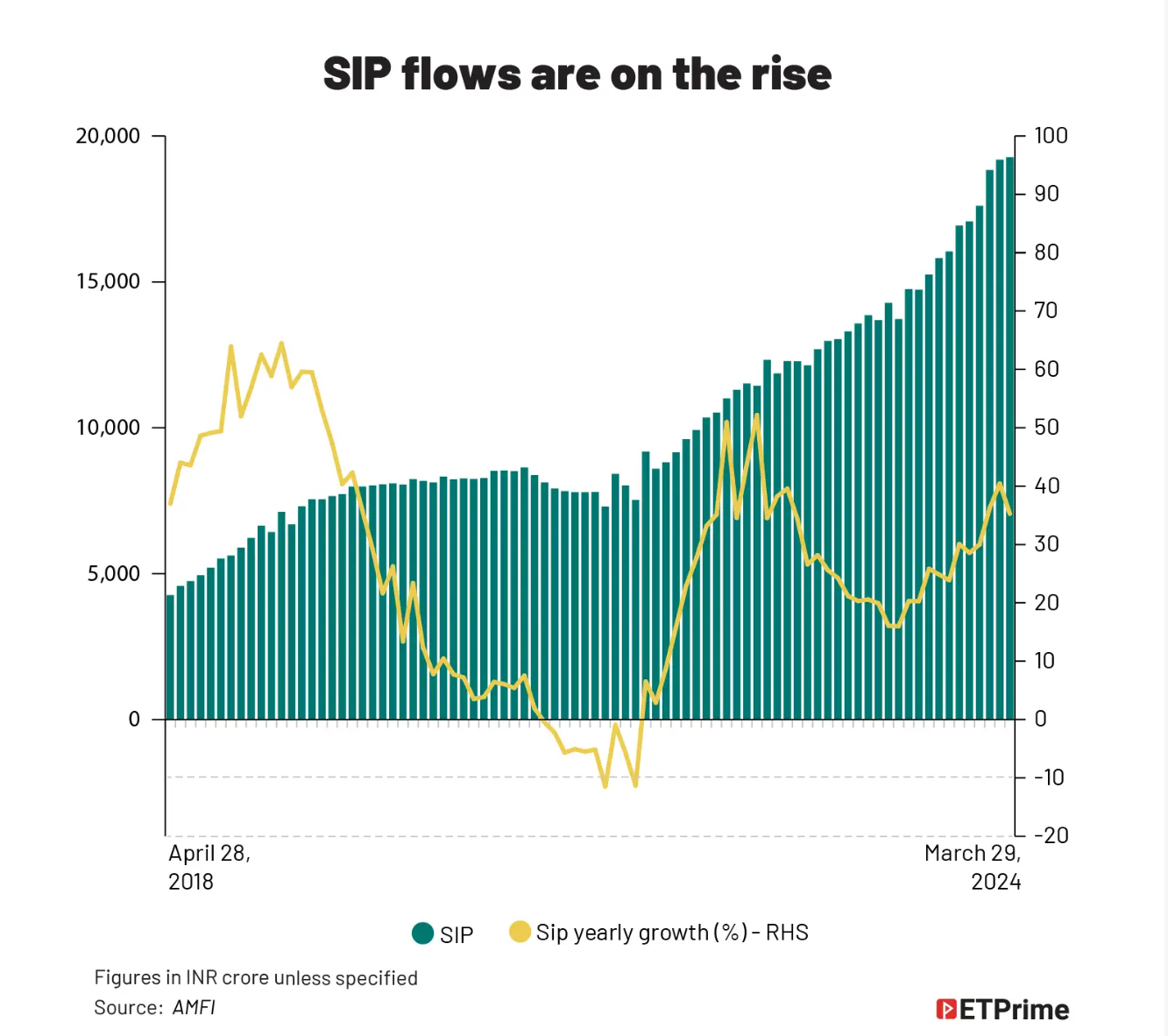

SIP trend in the recent past has been revolutionary. The number of demat accounts today are at 140 million. In a nation of nearly 500 million working population, the penetration is now nearly 30%. If this gets to 50%, we’ll get to the peak levels achieved in developed markets.

The SIP flows were around INR8,500 crore per month before pandemic. After March 2020, the flows dipped for a while in an uncertain environment. However, most money continued with discipline. This was welcome news.

There are few challenges though that need attention.

Firstly, most growth in new SIP accounts happened in 2021 when markets were at peak valuations. Flows per month peaked in October 2021 just as the markets did then. So marginal money is trying to time the market even on SIP mode.

There is another side to the SIP story that is concerning. SIPs are getting closed at rapid pace indicating lack of conviction by almost half of the customers. The FY20 had a total of 31 million SIP accounts. This increased to 63 million by FY23 and 83 million by FY24. But to get to the additional incremental 20 million SIP accounts, the industry had to open almost 43 million new accounts. So, almost 23 million accounts were closed or deactivated.

That implies that a good 25% of overall SIP accounts base were closed in last one year. Even if these folios closed and moved to another fund, the trend is defeating the purpose of SIPs.

Is the SIP story real or just another flavour of chasing returns if the going is good?

So how many unique customers have stayed since 2020? Research on that is limited. Certainly, much less advertised by fund houses that have folio-wise data. But there is a new twist that may ruin the SIP story in unexpected ways. It will also test the patience of committed SIP-pers in ways not seen before.

Chasing past returns?

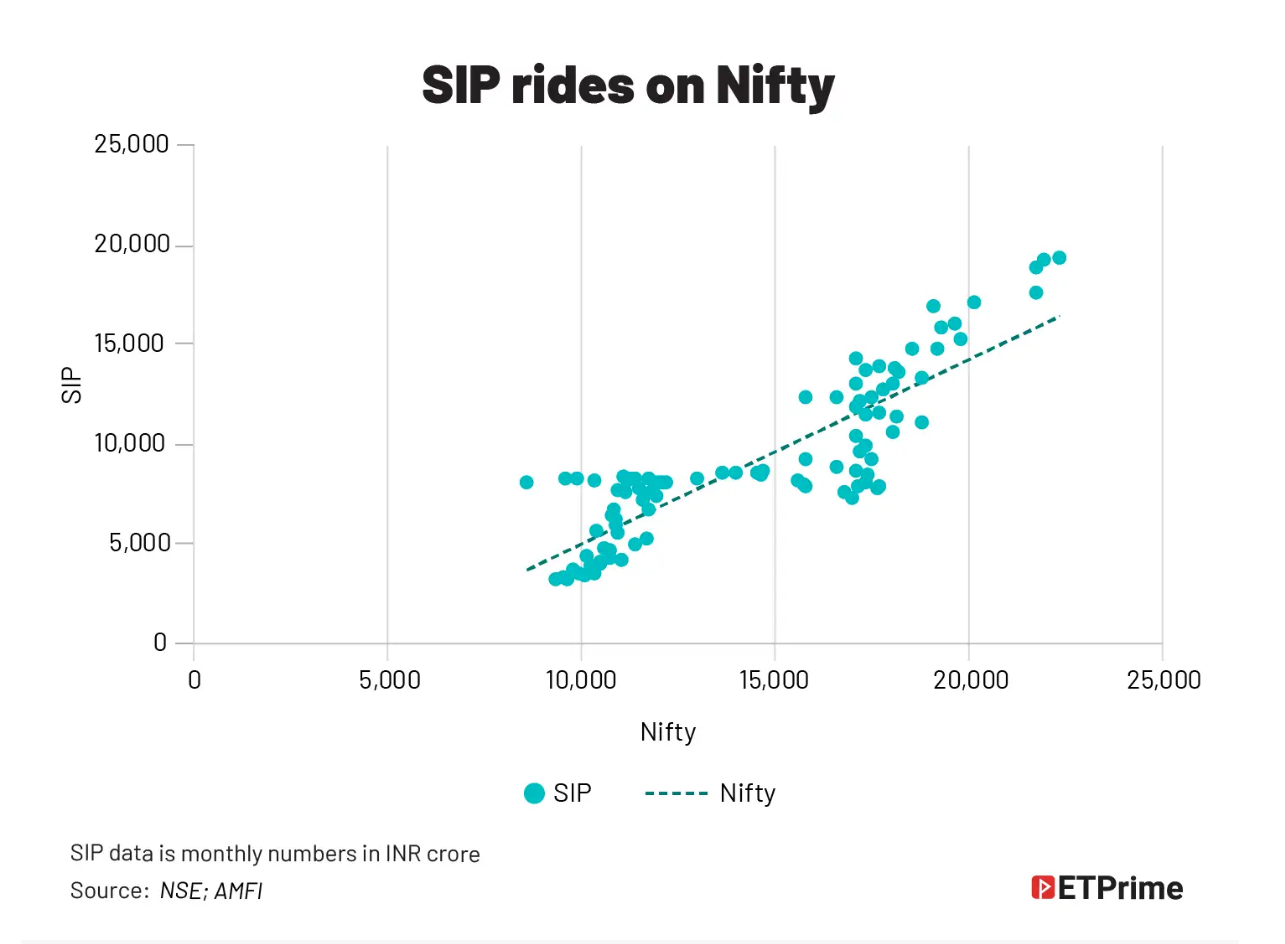

New SIP accounts are closely linked on the movement of the Nifty 50 and have a very strong correlation or R square of 75%. For every 10% move in the Nifty, SIP flow will likely increase by 9.2%. But what is more interesting is that if the market goes flat or simply doesn’t move up for say more than a year, the SIP flows will begin to dip immediately. Let’s examine this a bit more.

AMFI reports indicate that the number of folios (SIP and others) in equity and hybrid schemes in March 2021 was 75 million but spiked to almost 136 million by March 2024. So, the customer accounts doubled in three years but all at peak valuations after 2021. What’s worse, while large-cap folios have increased by just 30% since FY21, we see mid- and sectoral-fund folio count increasing by 210% and 230%, respectively.

Small-cap SIP accounts increased by a whopping 380% after FY21 and are now 50% more than large-cap accounts. What kind of SIP education is this?

The SIP flows number is the highest ever at INR20,371 crore (USD2 billion) per month for April 2024. While that inspires confidence in markets, the shocker is the huge shift towards mid- and small-cap funds. Since mid-2022, large-cap funds have begun to see outflows that accelerated in 2023. The AUMs of large-cap funds are INR3.1 lakh crore, which is equal to mid-cap AUM. Small-cap funds at INR2.5 lakh crore AUM are not far behind. This skewed proportion clearly indicates that the old style of investing based on past returns in back. Just that its form has changed to the SIP mode.

Choice of the crowd converges to average

While systematic investing may prevent steep drops in invested capital for clients, it may well be the case that they are closing large-cap folios and opening mid- or small-cap accounts. The data certainly indicates that. No wonder, many mutual funds have decided to stop accepting lumpsum investments in small cap. Because the money for small-cap funds is not fresh capital. It probably was coming from redemption of large-cap funds from the same fund house.

It is tempting to time the funds based on past returns, especially when the existing kitty looks large enough. In the coming years, we’ll increasingly see customers falling to this trap. Until now, the SIP-pers haven’t really got the fruits of their discipline since it takes time to accumulate corpus, especially when most purchase has happened at peak prices.

Additionally, most of the SIP flows have been spent in buying same stocks at high valuations where the foreign investors have made a smart exit. FII holding has dropped from 22% pre-pandemic to almost 16% now. When large-cap funds stay stagnant for a couple of years, the patience of SIP investors will be tested. And most are likely to relent.

Why isn’t the previous generation rich?

Let’s come back to the original question. Why don’t we see enough people from the previous generation who have got rich from equity investing in 1990s to 2010s? That’s because it is never so easy. Markets rarely behave like formulae. They test you in new ways. When past returns drive current choices, the space gets crowded soon enough. This causes prices to rise to levels at which the past returns don’t work. So, you will make some money but not what is being projected by most. Not much different than the previous generation made.

Couple of decades from today, your working-age children will ask – Dad, why didn’t you make money in markets? Had you invested XYZ amount in such and such fund for 20 years via this new AI-based exotic SIP, you would be sitting on XYZ millions.

You may not have a perfect answer, but you will certainly smile.

The article first appeared for The Economic Times in May 2024.