India Market Outlook - 2025 & Beyond

Dec 29, 2024 - Anurag Singh

10 points on India Outlook for 2025 & beyond

Indian Markets: 10 Key Takeaways & Outlook FY 2025

1. There is no reason to panic. However, reset your expectations: #nifty50 was 12,000 in 2020 Jan, pre covid. At 12% growth, it should double in 6 years. So 24,000 by 2025 is still fine. Expect the same result in 2025 & absorption of the post pandemic gains. Mean reversion is one of the ultimate truths in markets. What is the mean return ? The 30 year Nifty historical returns are at 11% for Nifty 50 & 10% for #Nifty500 (Doesn’t include dividends). So returns from Nifty 500 are 1% below Nifty50. This implies that mid & small cap perform much below large caps in the long run. So those who think mid-caps & small caps would beat this benchmark, think again. This hasn’t turned out that way in India over 25 years till 2019. If you’re betting for mid & small caps & against large caps, you are betting against history.

2. Earnings growth was good for 4 years but is cyclical: Earnings growth is moderating & Nifty 500 topline growth is struggling at 7% for last one year. Markets should take correction when due. The NIFTY EPS has risen from INR 430 (Jan 2020) to INR 950 (Jan 2024) in 4 years (CAGR of 22%). The markets though have accounted too much exuberance & have failed to recognize that this EPS growth is not sustainable. A confluence of factors resulted in earnings growth post 2020 – Banks balance sheet cleanup, IT demand surge in US, Discretionary revenge spending post covid & finally the govt capex increasing 4 times to 11 lac cr. All that is behind us now. EPS estimates for Nifty 500 is at 7% for FY25. There is no reason that we stay at valuations that were projecting earlier with 20% growth estimates. Look at some history here. Indian corporate profits rose from 3 lac cr to 4 lac cr ($47 BN) between 2010 to 2020 so hardly 3% growth. However from 2020 to 2024, the profits quadrupled to 15 lac crore ($ 180 BN). The results of Unilever & Bajaj Auto in Q2 2024 are enough to convince us that the earnings can’t grow at 20% in a moderate growth environment. Why is Unilever valued at 50-60 PE when topline grows at 2% (including inflation)? The only fair value is in top private banks. Ironically, very few are interested there.

3. Indian valuations are really high (Beyond Nifty50) - just be aware of it: In sept 2024 peak, 50% of the Nifty 500 stocks were above a PE of 50. This is unlike anything seen in any major financial market globally. In 2008 at the height of GFC bubble, only 15% of the stocks in India were above 50 PE (When nominal GDP growth was 15% plus). So, while 2008 was earnings driven rally, the current one is largely a multiple expansion. Buying at these valuations (25 PE plus) diminishes your returns for next 5 years. It is going to happen anyway. Just be aware. This time is not different. Even though you may believe that it is.

4. $5 TN market cap for India is way too excessive. Some global comparisons are in order here. India market cap to GDP is 150% now & has crossed the #WarrenBuffett fair valuation zone of 100%. Compare this with UK $ 3 TN, France $ 2.8 TN, Germany $2.2 TN. There is no reason why India should be valued that high compared to other similar sized economies. Justified levels for Indian markets should be around 100% of GDP ie at $3.5 TN or max $ 4 TN. Anything above that is froth on account of domestic fund flows. This doesn’t mean that markets could correct soon. However in a decade, anything bought around these levels is not worth the returns you get. Markets certainly will find their fair level by the end of this decade ie by 2030. Why does the over-valuation happen in Indian markets? Because India has strong capital controls. It doesn’t allow you to invest freely in US or global markets. This is not the case with most developed markets like UK where you can invest 100% of your money in US, no questions asked. You can’t do that in India.

5. India story is intact. It is growing at 10% nominal: India story is intact. And growing. But it’s growing at 10% nominal rate. Regardless of the debate every quarter, this average has held good since 2014. So the markets could expect a 12% CAGR on large cap companies. This implies that reversion to mean is imminent. Just as a reference, the nominal growth rate of GDP between 2003-2008 was 14.5%. No wonder the stocks reflected a buoyancy on the back on high inflation plus earnings. We don’t have high inflation now. So returns will also moderate accordingly.

6. Market ownership in India (2024): Indian markets are heavily owned by promotors which leaves only 50% free float. It creates a limited supply & pushes prices up. As of 2024 the holdings are: Promotors 52% (including 12% govt), Retail + HNIs 25% (including MFs & insurance), Others 6%(NPS, EPFO, private trusts) & FIIs 17%. Not to forget that some FII holdings too may be promoter money in a different name. The only sellers in India are the FIIs. DIIs are forced buyers when domestic funds continue unabated. It’s a difficult place for a value investor. Moreover, most overvaluation is in mid & small caps where FIIs are absent. So domestic money which can’t flow outside India keeps buying the same stocks to ridiculous prices. There is no value here. This is pure herd buying. Don’t justify this in the name of growth. Just be aware that it is more money chasing fewer stocks. All MNCs are aware of this arbitrage. They will capture this free money.

7. Why are FIIs selling? Invert the question - Why are domestic investors buying? The debate of #FIIs selling is a distraction. The bigger concern is significant promoters selling, private equity selling & listing via insanely priced #IPOs & #QIPs. That is the real red flag. Who is the conscience keeper here for domestic investors? Forced buying doesn’t get the right price. In 2024,almost $35 BN has been sold by FIIs. Another significant amount of appx $30 BN has been sold by Indian promotors & private equity firms via QIPs & fresh issuance. Hyundai raised $ 3.3 Bn overnight & we are very happy to let them walk away with it when across the globe, auto companies are at single digit multiples. When Zomato says that they will get the foreign capital to below 50%, that is like taking money out of India. Why don’t we question that? Why are you buying these stories with no serious profit prospects? You always have a choice.

8. India is running on one in a lifetime bonanza for next 20 years: India has added 25% population in each of the decades ending 1980 & 1990. Those cohorts are turning in their 30s & 40s now. This is the period of “maximum spending” in a person’s lifetime. The 80s generation will turn 50 by 2030 & has good spending period ahead. With median age at 30 years, 50% of the population is in peak spending stage & this will keep demand going for real estate, cars, consumer durables, travel & tourism, hotels, etc. No wonder you find everything so crowded. This is a great setup for organized listed players. And the once in a lifetime opportunity for a nation to rise.

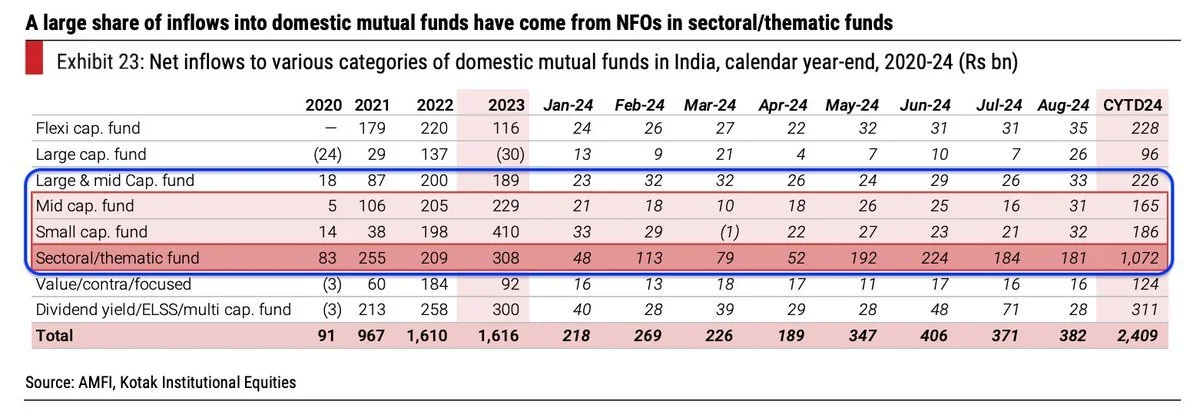

9. Continue that SIP but also re-evaluate your portfolio allocations: First question: What kind of an investor are you? If you sold out during covid fall, you are not an aggressive investor. If you have entered after 2020, you certainly haven’t seen enough of markets. Make a self-assessment. If you’re feeling more than 10% pain, look at your SIP portfolio. Because your portfolios may be misaligned or mis allocated to India story. You may be chasing the past returns, which is the classic bull market trap. Your long term portfolio should be 50% in Large Caps, 30% in Mid/Small caps & balance 20% in debt instruments/PPF/FDs. Count flexi cap as something between large & mid/small caps. Thematic funds are certainly in mid/small cap risk bucket, perhaps riskier. Add to that your risk tolerance & make adjustments. Nearly 75% of current Indian investors have entered after 2020. This is a bit precarious too as they have not yet seen a bear market. They are also chasing mid & small caps as we see in graphic below. Will the behavior of new generation different when bear market hits?

10. Long term, the markets will behave the way they always do. Take time to absorb this. Indian market returns are likely to be 12% appx in the long term. Mid & small caps returns are likely to be lower at 10% appx. That is what history says. Anything more or less will get averaged out. We just don’t know when. So don’t fear these corrections. Ask yourself – what returns do you expect ? Some will blink during market drops, thereby creating opportunity for the rest to stay invested. Pray that the markets correct soon enough. If markets stay expensive next few years, then the rich guys gain more. If they stay cheap & rise in future, SIP investors have better change to get rich. So celebrate the correction & stay invested. That is the only way the SIP investor can win. Best wishes for a prosperous 2025 & beyond.