US Markets: Outlook FY 2025

Dec 30, 2024 - Anurag Singh

FY 2024 Year End Update & Outlook FY 2025

1. US Exceptionalism continues & Trump victory has intensified it: S&P500 returns for FY24 are 26% which is phenomenal considering FY23 returns were at 24%. Will the third time lucky play out? Chances are more likely than not. It may not be as large but with EPS projections at $275, S&P is at 22 forward PE, S&P is not too expensive to warrant a correction. Additionally don’t forget that 2022 at (-20%) so the cumulative growth over 5 years since 2020 is 15%. This is great but not over the board considering the inflation spike as well. Nasdaq surged 34% this year on the back of 44% in FY23. Nearly 37% of the entire market cap in concentrated in just 7 stocks. While this concentration is unprecedented, so is the domination of these firms. There is no clear competition in sight, for now. US equity funds see inflows of $ 150 BN since Nov 5th. Funds that invest in emerging markets have suffered net withdrawals of $8bn since the election, including around $4bn exiting China-focused funds. Those that invest in western Europe have lost around $14bn and Japan-focused funds lost around $6bn, according to EPFR. (FT reports).

2. S&P500 EPS estimates are at $275 for FY 2025 that brings S&P 500 at 22x forward multiples. Broadening of rally underway for the other 493 stocks outside of the 7 Big Tech stocks. The sectors to gain are financials, Industrials, communication services & consumer discretionary. This can be seen when 80% of the #SPX500 stocks are above their 200 day moving average. Outside of big tech that have stagnated (Except Meta & Amazon), the rest of market is 100% of GDP, so very fairly valued. Valuations continue to be very depressed in Russell. But Russel has always been a stock pickers market in a rangebound index. A larger question confronting mega-tech stocks is this: Is the #AI story real & what is the ROI? Estimates vary on how much jobs AI can replace from 5% to 65%. Take your pick (GPUs , LLMs, Quantum computing) . Earnings growth differential for Mag 7 vs the rest has been shrinking now: 2023 had a 64% delta, 2024 was 32% delta & in 2025, big-tech EPS is likely to grow just 4% ahead of the rest 493 stocks. (Goldman Sachs estimates). Will valuations correct? That may decide the headline returns from S&P500 in FY 2025.

3. NVIDIA Frenzy continues but losing steam: #NVIDIA Q3 2024 results: Revenues beat at $35 BN vs 33 BN expected. Revenue guidance for current Q4 is $37 BN. So we see a slowdown in the beats now. It is all in the price when a company with topline of $140 BN is trading at $3.6 TN (Price $150) ie 25x sales. While it was able to double the price & increase margins to 80%, it will come down gradually as competition emerges & people question the ROI from AI. At the peak valuation of $3 TN, NVIDIA weight in index S&P500 was 6.3%. It was bigger than 5 sectors ie Consumer Staples 6%, Energy 5%, Utilities 2.4%, Real estate 2.4% & Materials 2.2%. NVIDIA data centers revenue grow from $4.3 BN in Q1 2024 to $10 BN (Q2), $14 BN (Q3), $18 BN (Q4 2024) & $22 BN in Q1 2025. At some point in history, we’ll look back at this & wonder in surprise – Why did we value this stock so much? How could we?

4. Federal Reserve’s fight on inflation in nearing its end: The FOMC rates are now at 4.25% - 4.50% range, dropping 100 bps since the rate cuts started in sept. Chair #Powell began the rate cut on Sept 18th 2024: Fed did a 50 bps cut. The 50 bps cut was probably a catch up to the current 10 year yield & the missed opportunity in July for a 25 bps since the Aug jobs data was received later. The ISM PMIs have contracted to 48 for manufacturing & 51 for services. As we stand today, the risks to employment market are higher vs risks to inflation. New jobs addition avg for last 12 months is 190 K. However most jobs are in healthcare & social services which are largely temporary jobs. Unemployment stays strong at 4.2% but #FederalReserve would not like to risk any further from here. Wage growth is also at 4.0% which is closer to the long term average of 3% or below. It is stuck here for a while but likely to get there. Continued claims also are at 1.9 MN which is right where they should be (pre 2019) in a long term trend. The economy is in a very strong place & our intention is to keep it there (Powell).

5. US 10 year yield – New normal is 4%: Currently at 4.25% - 4.50% broadly aligned with 10 year yield. For FY25, we may end up in the range of 3.8% to 4.5% for US 10 year yield. This make a new normal for the housing market that will have to get used to the sub 4% mortgage rates post 2008. Mortgage applications are broadly 50% down during 2024 from the peak of 2021 that saw nearly 300K applications per week. The high yield has an external impact too on money flows. It adversely impacts the emerging market flows as we are not going back to zero rate regime. 10 yr may eventually settle at 3.5% in the medium term. #FOMC projection is at 3.9% with inflation at 2.5% by 2025 end. It is very likely that they may have to wait at 3.5% FOMC rates in the medium term until inflationary pressures wane. That leaves just about 50 bps ie 2 more cuts to go till 2025 end. In any case, #Fed is sitting on a lot of dry powder should the labor market weaken, subject to reasonable inflation control.

6. World Peace ? Geo-politics is likely to get better with Trump administration: With #Trump presidency & US policy of not engaging in un-necessary wars, it is very likely that faster settlement may be reached in the Russia-Ukraine war. Israel is also expected to get stronger support which may bring a faster settlement & peace in the middle east region. At-least for the medium term. This is better for global energy markets & international trade. This may also be a good tradeoff for tariff negotiation with the rest of the world. A peaceful world is good for everyone.

7. Global stimulus bonanza - 80% of Global Economies are in stimulus mode (Post inflation control) - Rate cuts are underway in US, EU & China. Stimulus can take any form, Monetary, Fiscal & Investments or even defense spending. With 80% of global economies in a stimulus mode & no credit crisis, the world economy will do well. Expect more demand side measures in #EU (monetary rate cuts) & China economy (monetary, fiscal & structural). US is expected to stimulate economy via tax cuts & regulatory easing. Remember the #DOGE effort by Musk & Vivek. It would be the most interesting political watch-out for FY25. US govt is deficit spending at 6% of GDP which is a key contributor to inflation too. At a national debt of 100% of GDP, the spending path is clearly not sustainable, as noted by Fed Chair Powell. This is the biggest peacetime binge that must stop.

8. European Central Bank faces an uphill task: #ECB will continue to cut interest rates to avert unnecessary damage to the economy. The central bank’s governing council decided to cut rates by 0.25 percentage points to 3.00%. It argued in Oct 24 that “the disinflationary trend was getting stronger” and that it was important to avoid “harming the real economy by more than was necessary”. Europe’s problems will now be compounded by the Trump tariffs which will add further pressure on the Eurozone economy with only very modest GDP growth expected in 2025. The absence of growth will translate into bigger government deficits and political instability. European equities are cheap against their history. There are many good and well-managed companies. But they are in the wrong domicile and will be targeted with increasingly high tax rates by failing governments. Despite the relatively low valuations, European equity markets will continue to underperform. #FT reports

9. Buffet goes 55% cash in 2024. Should you ? #WarrenBuffet sold $130 BN of stock last quarter including $110 BN of Apple. Current holdings are $325 BN cash, $280 BN equities. Of which Apple is still $70 BN. (Total $600 BN). His stellar record of 20% annualised returns over 60 years looks impossible to beat. May be he’s trying to preserve that. Large companies are priced to perfection. US tax rates may go up & debt levels indicate higher interest rates (so lower valuations). #Buffet said, “I think when I look at the alternative of what’s available in the equity markets and I look at the composition of what’s going on in the world, we find staying in cash quite attractive”. Berkshire reported that it had generated gains of $97 Bn on the $133 Bn of stock it has sold this year, which after taxes amounted to a $76.5bn pay-off for the group. Should you feel the same? Probably not. Recognize that Berkshire has what I call “the problem of Billions”. At that scale, opportunities are limited & you have more dollars invested vs incremental flow. If you’re rich, it pays to stay in cash or bonds & preserve current wealth with risk-off approach. Buffet will still earn risk free 5% on $325 Bn which is $16 Bn annually. The average investor doesn’t have the problem of billions. In short, what works for Buffett may not work for you. He has too much to lose in case of a market crash.

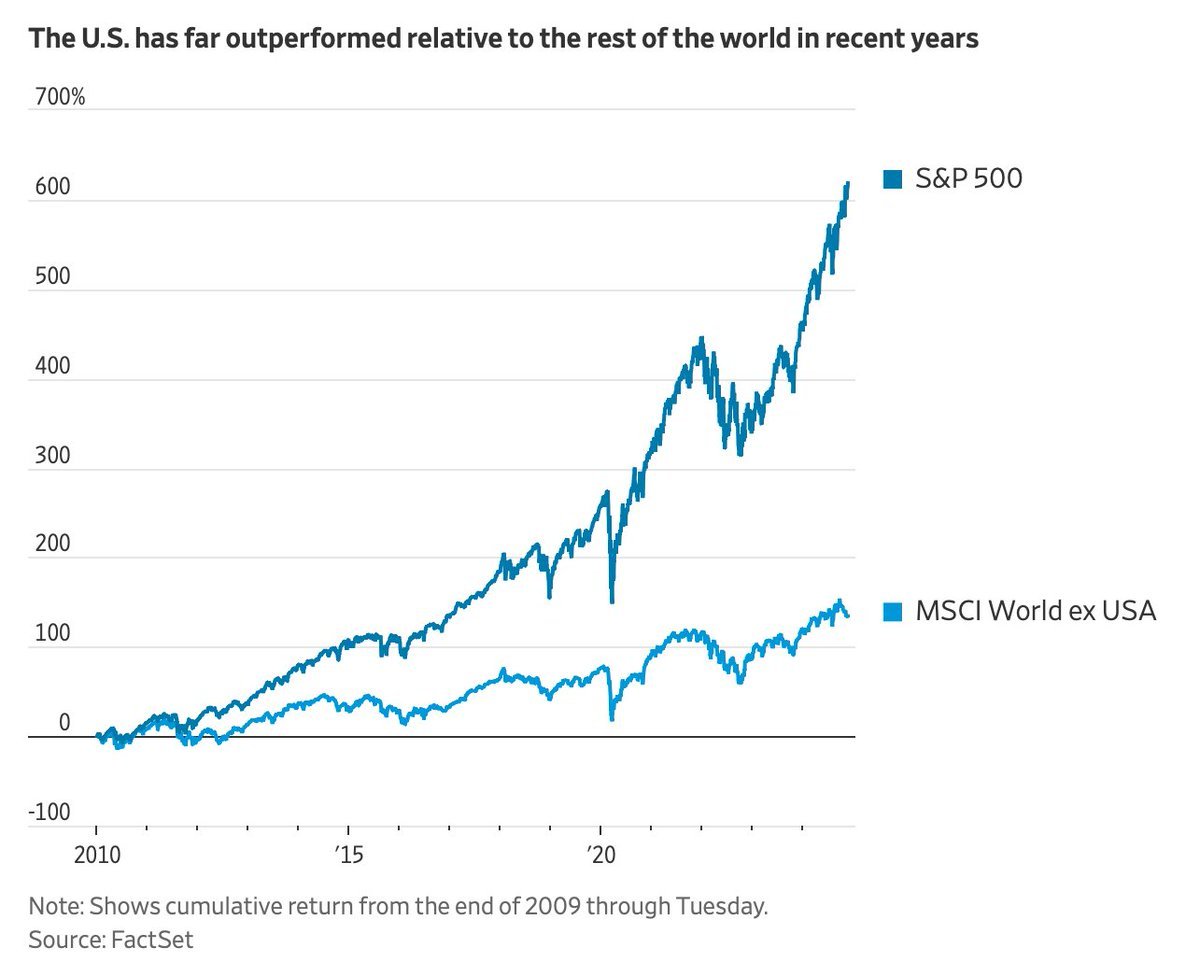

10. Dominance of US in MSCI World post 20010: The below chart best captures the US dominance vs rest of the world. #MSCI World Index had a weightage of 58% for International markets in 2010. The Weightage has been steadily coming down & is now at 33% only. The gradual decline in international allocation is due to EU economy stagnating & US regaining on tech strength. Finally China doing a self-goal & not proving to be an investor friendly markets as many thought. May be that was by design as they like capitalism of jobs creation but not financial engineering where a very few make money. Also many believe that 30% to 40% of US earnings come from international markets & stocks like Google, Meta, MSFT, AAPL, Amazon, Even McD, Starbucks & NIKE are in a way an exposure to global economies. US funds don’t need international exposure anymore. Meanwhile, #Argentina ETF (ARGT) has grown 45% YTD & 100% since #JavierMilei took power. Nothing is permanent. Valuation matters, always.

Best Wishes for 2025.